Jersey City’s Enron Moment: Lessons to Learn

Earlier this year, Mayor Solomon published a 24-page diss track, accusing ex-Mayor Fulop’s administration of dishonesty, disloyalty and disinterest to the tune of $250M. While we don’t agree with all of the mayor’s conclusions, the core claim that Jersey City’s finances have been mismanaged is clearly warranted.

In other contexts, we might be able to compel the former mayor and senior administration officials to come forward and explain themselves (or else). That’s what happened 20 years ago when Enron executives did what Mayor Solomon is accusing here. There, senior Enron executives used creative accounting to give investors the impression the business was doing better than it was. Upon discovery, the guilty executives were sentenced to prison and had their assets seized, and the people who were supposed to (but failed to) oversee those executives faced serious professional and personal financial consequences.

Because this is the public sector, so nobody here will likely see any consequences. But we can at least take some important lessons from the affair to make sure it doesn’t happen again.

The Failure Was System Wide

While Mayor Solomon has largely pointed the finger at his predecessor, it’s important to remember that in Jersey City, the mayor isn’t actually responsible for the budget! The budget is the city council’s job, and the things proven true about financial fraud here generally fall on their shoulders.

In Enron, the board of directors, roughly equivalent to our city council, ended up paying $13M out of pocket for not catching the fraud earlier. It could have been much worse for them. They escaped criminal prosecution largely by pleading ignorance. They argued that (i) they believed the company’s executives were honest and (ii) Enron had independent auditors who should have, but failed, to tell them there were problems, so it was really their fault.

While the Solomon Report indicates that our city council was misled like Enron’s, our council had much more reason to suspect something was amiss, especially because the city’s independent auditors told them as much. Repeatedly. Key evidence below:

The city’s finance department for years missed spending estimates (nearly always in ways that made the city’s books look better), leading the city’s auditor to declare the city’s financial reporting “not reliable.”

Between 2015 and 2024, Hoboken’s auditor asserted a single significant financial reporting error requiring correction (for a procedural oversight). By comparison, in that same period, Jersey City’s auditor identified scores of serious omissions and errors in 7 separate years, some repeated year after year.

Both internal and external whistleblowers made credible claims over years about Jersey City’s weak financial controls—to the point of publicly questioning whether the city’s extreme financial errors could plausibly have been accidents.

According to reporting, the city’s credit rating was downgraded in 2024 in part because the ratings agency didn’t trust the city’s financial reporting.

The signs were there. Stunningly, in spite of them, the council apparently did nothing. We are not aware of a single public hearing the council undertook to critically investigate the city’s books. Instead, most of the council appears to have simply checked out of its oversight job.

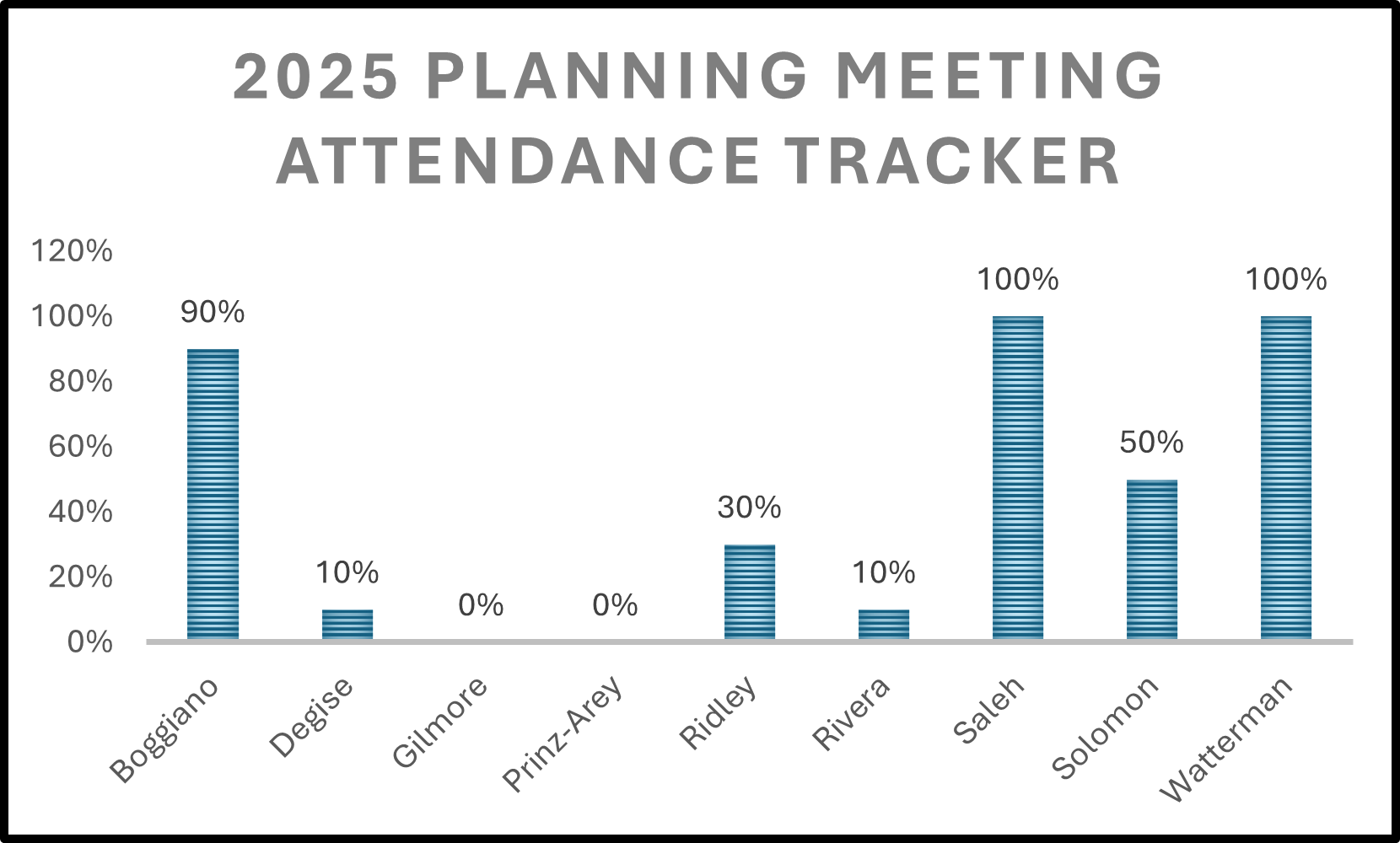

Above, a disheartening look at how little ownership the council took over financial matters that were their responsibility to get right.

By our count, for example, the average 2025 budget hearing had 50% attendance. Multiple councilmembers have gone years without making a single substantive budget comment.

The state government likewise should have seriously considered stepping in to provide stronger oversight. The state has the power to take over financial decision making in troubled municipalities, and it should have looked closely at Jersey City’s. Again, the signs were there.

An important caveat: then-Councilman Solomon gets high marks here. While on the council, he was the loudest and most regular voice pointing out the city’s financial missteps. If the full council took their oversight responsibilities as seriously as Councilman Solomon, we wouldn’t be here today.

What We Can Learn From Enron

Enron was the catalyst for significant reform of US financial oversight over large companies. In its wake, Congress passed Sarbanes-Oxley, empowering financial regulators to require transparent reporting and deliver consequences to those who didn’t. While public sector officials aren’t held to the same standard, we can implement the spirit of some of the post-Enron reforms. Hopes for each stakeholder group below:

The City Council:

Empanel a citizen’s budget committee to advise you, as state law empowers you to do. Understanding the budget is difficult, but the city has a citizenry brimming with experience in financial management to help you. Lean on them.

You’re empowered to demand the budget be delivered on time and in an easily-digestible format, or else. Make that the norm.

Set clear departmental performance goals and use your powers to ensure those goals are met. You are responsible for setting taxes, so you should take ownership for making sure tax dollars are well spent.

City Hall:

Be a better partner to the council. Provide them clear and timely communication about spending and performance. Not like this.

State Government

Take a more active oversight role. The threat of your action will deter dishonesty.

Voters:

It’s generally actually easier to mislead about performance than spending. If your government can blatantly mislead you about spending, can you blindly trust that it’s doing a fair job delivering services with that money? Demand answers about performance too!

While we’re encouraged that voters recently voted in a council with more financial and professional experience, we’re far behind Hoboken and other better-run cities in professionalizing the top ranks of our government.